What would the insurance reforms in the federal healthcare bill mean to us New Yorkers.

He stated that the ‘system’ wouldn’t change much in New York because the bill proposes extending the New York ‘system’ to the rest of the country. For example:

- In New York a policy is guaranteed issue - a company can't decline you due to your health,

- In most cases pre-existing conditions are already covered - in most areas of the country a health insurer requires a medical exam, and an insurance company can decline you for coverage

I asked about HSA’s and why they are not more popular. I learned that HSAs are both good and bad. They are advantageous because the premium is less expensive then most other options (HMO, EPOs, PPOs). But, the premium savings often isn't enough to justify the purchase of an HSA.

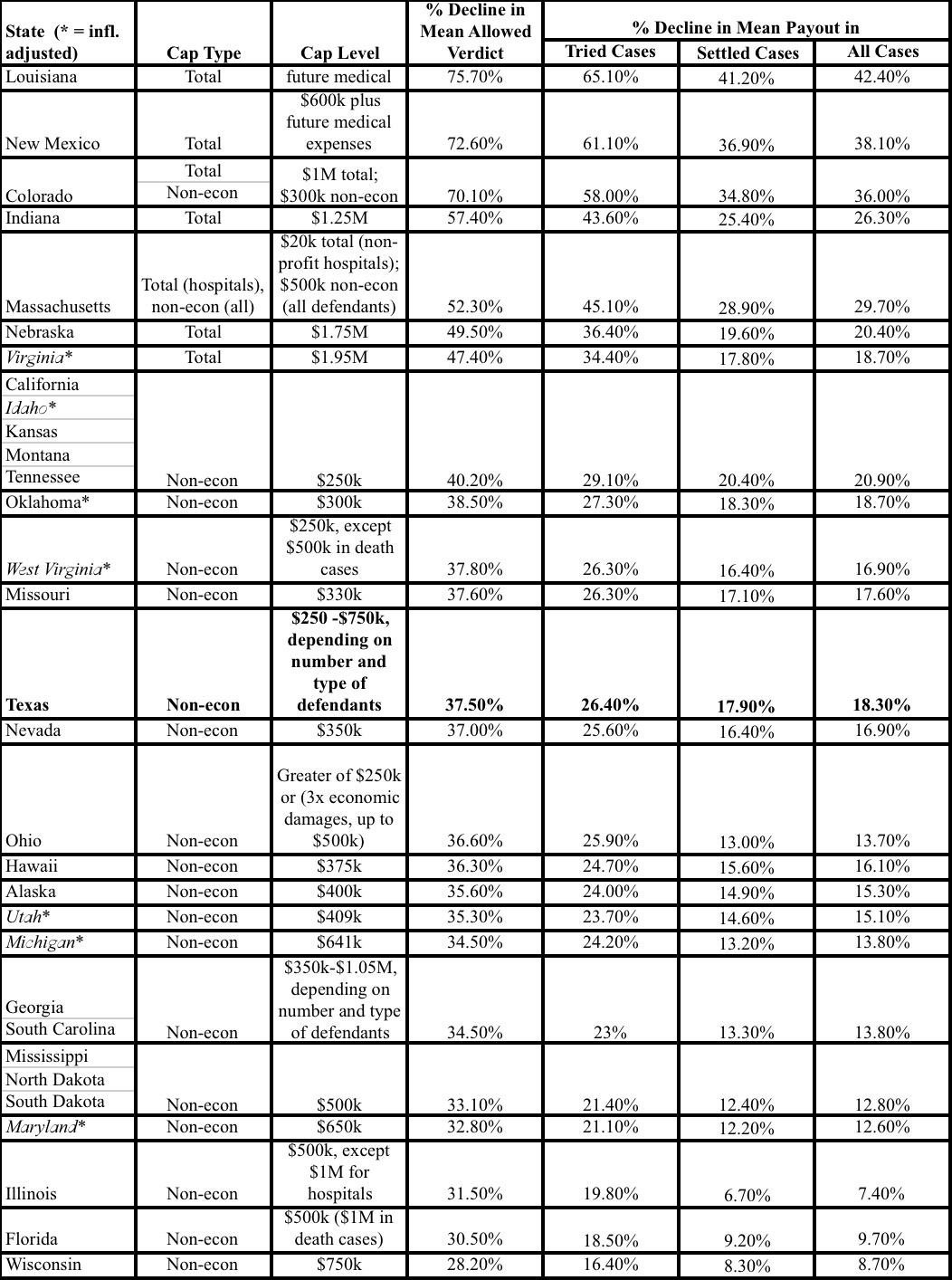

He stressed that insurance reforms alone are merely a component of HCR. He stated that needed reform also included tort reform, obesity issues, etc

link to health insurance protections

{kind=link}

The most important obesity issue will be the size of the bloated bureaucracy created by the federal government.

ReplyDeleteFunny. But please lighten up and stay on topic - preserves the value of this blog for all of us

ReplyDeletethanks

from white house.gov:

ReplyDeletehttp://www.whitehouse.gov/assets/documents/health_insurance_consumer_protections.pdf

The most important feature of the HSA is that the patient/consumer has control over his healthcare dollar. That is precisely why folks are worried about this government's plans. They say they didn't want to be in the auto business but they now run GM and Chrysler. Now they say they don't want to run Healthcare. Why do I hear the voice of Joe Isuzu?

ReplyDeletetrue, that is a good feature, 'control'.

ReplyDeletebut two concerns exist:

1) is this 'control' (actually consumer direction, not quite control) that the consumer gets via an hsa, more than offset by the adverse behavior of a typical(insurance company) intermediary.

2) when the consumer lacks the medical expertise or lacks adequate funds, how meaningful is their 'control' or 'choice' in reality?

(again, the gm/chrysler - govt thing is beyond the scope of this post on hsa's. i'm happy to respond to that - let's just start a new post)

END COORDINATION OF BENEFITS

ReplyDeletewhy doesn't the reform proposal collapse no-fault and workers comp into the fold - everyone would have the coverage of their choice but only one coverage, no more 'coordination of benefits'.